How Much Money You Have To Pay A Month In Mortage For A Million Dollar Home

Await to need at least $100K of income for a $1M home

At that place'southward no magic formula that says you need 10 income to beget a $one one thousand thousand firm. Because income is just function of the equation.

With a actually stiff financial profile — high credit, low debts, big savings — you might afford a $1 million dwelling with an income around $100K.

Merely if your finances aren't quite as potent, you might need an income upwardly of $225K per year to buy that meg-dollar domicile.

Wondering how much house you can afford? Here'south how you can find out.

In this commodity (Skip to...)

- Income to beget a meg dollar home

- Income examples

- Calculate your domicile buying budget

- Don't forget about homeownership costs

- Benefits of buying a $1M business firm

- Today's mortgage rates

Household income to afford a million-dollar dwelling house

There's no "magic" income number to afford a one thousand thousand dollar house.

In reality, it'south possible to buy a $1million home with a variety of income levels. That'due south because your dwelling house-ownership budget depends on other factors, as well, like your down payment, debt-to-income ratio, and mortgage charge per unit.

Accept a wait at the table below for a quick overview of how these factors, combined with your salary, can bear upon your 1000000 dollar habitation purchase:

| Annual bacon | Down Payment | Monthly debt | Involvement Charge per unit* | Monthly payment |

| $147,000 | xx% | ≤ $250 | ii.75% | $4,100 |

| $224,000 | 20% | ≤ $2,500 | 2.75% | $4,220 |

| $224,000 | 20% | ≤ $two,500 | three.00% | $4,252 |

| $110,000 | l% | ≤ $250 | 2.75% | $2,900 |

*Estimates based on 30-year fixed-charge per unit loan, property revenue enhancement charge per unit at 0.97% annually, dwelling house insurance premium of $600 per year, and no HOA dues. Involvement rates are for examples purposes simply. Your own interest rate volition be dissimilar.

A million dollars was once a lot of coin to pay for a home, and unless you lived in Los Angeles or San Francisco, you probably would never consider purchasing one.

But as habitation values continue to skyrocket beyond the country, one thousand thousand-dollar homes are becoming more common outside of California and New York. The good news is that you don't need to be a millionaire to afford one. But you lot should have your personal finances in society to ensure you get the best charge per unit.

Examples: How much yous have to make to afford a million-dollar home

Monthly income is but one factor in your home buying budget. The purchase price you can afford also depends on your:

- Debt-to-income ratio (DTI)

- Credit score

- Down payment amount

- Mortgage rate

We experimented with a few of these factors using our home affordability calculator to show you how much each one can affect your budget.

Prime borrower: $147,000 income needed

Our commencement example looks at a traditional 'prime' borrower (one with excellent credit and strong finances). They have:

- A 20% downwards payment ($200,000)

- Only $250 in pre-existing monthly debts

- An excellent mortgage charge per unit of 2.75%

This borrower tin can afford a $1 million dollar house with an annual salary of $147,000. Their monthly mortgage payment would be nearly $four,100.

Loan summary:

- Purchase toll: $1 million

- Down payment: $500,000

- Loan amount: $500,000

- Loan term: thirty years

Monthly mortgage payment breakdown:

- Principle and involvement: $iii,266

- Monthly tax: $808

- Monthly insurance: $50

- Full: $4,124

High-DTI borrower: $224,000 income needed

Permit'southward leave everything else the same as in the offset example, but increment the borrower'due south monthly debt payments to $two,500.

For those paying multiple kid back up and alimony payments, that might be more realistic, fifty-fifty if their debts are only average.

And others have that level of debt payment even without family commitments. Retrieve luxury car, boat, motorhome, and other big-ticket toys.

In this scenario, the income needed to beget a home costing $1.031 million would be $224,000.

To afford a million-dollar dream home, you lot'd need a slightly higher down payment of $214,000. And monthly payments would cost almost $4,220.

Clearly, existing total debt makes a big difference in abode affordability. Your salary needs to exist $77,000 higher to buy a home at the same toll point.

Lower credit borrower: $224,000 income needed

As a rule of thumb, a million-dollar purchase price will require a jumbo loan.

To get a jumbo loan, you lot typically demand a credit score of 700 or higher. But allow's say a borrower has a credit score on the lower end of the approvable range.

A lower credit score means they'll accept to pay a higher involvement rate than our earlier examples. We'll say iii.0% instead of the two.75% used earlier.

Loan summary

- Purchase price: $one,005,000*

- Down payment: $201,000

- Loan amount: $804,000

- Loan term: xxx years

Monthly payment breakdown

- Principle and interest: $3,390

- Monthly tax: $812

- Monthly insurance: $50

- Total: $4,252

That aforementioned $224,000 household income volition even so buy a $i million home, though the budget comes in at 1 at $1,005,000 rather than $1,031,000 — a full $25,000 lower. And that's still assuming $2,500 in monthly debt payments.

Allow's say you can beget a 50% down payment. Perhaps you've built upwards lots of equity as a long-standing homeowner. Or maybe y'all've had a windfall.

Chances are, in your happy fiscal position, yous've paid downwardly most of your total debt, and so we'll return that number to $250 in monthly debt repayment.

Loan summary

- Buy cost: $one million

- Down payment: $500,000

- Loan amount: $500,000

- Loan term: 30 years

Monthly payment breakdown

- Principle and interest: $2,041

- Monthly revenue enhancement: $808

- Monthly insurance: $l

- Total: $2,900

By putting downwards half the buy toll ($500,000) you can afford a $1 meg abode on an income of just $110,000.

Fifty-fifty putting down thirty% makes a big deviation compared to 20%.

With 30% down, y'all could potentially afford a $one,037,000 dwelling house on an income of $140,000. Compare that with needing an income near $150,000 if you put down but twenty%.

How to calculate your home buying upkeep

The best style to figure out your habitation ownership budget — curt of contacting a lender — is to utilise a mortgage computer.

This mortgage reckoner will help you figure out how much business firm you can afford based on your salary, down payment, and debts. It likewise accounts for other factors, like your mortgage interest charge per unit and estimated property taxes and homeowners insurance costs.

To get the best gauge, be as accurate as you can when filling out each field.

- Annual income: Your gross income from all sources earlier taxation

- Country: Your location tin affect the deal you'll get. And it will besides impact your property taxes

- Monthly debts: Minimum credit card payments, loan installments, car loans, student loans, plus alimony and kid support. In other words, all your inescapable, monthly financial obligations. Simply not things that vary, such as food, gas, utilities, and so on

- Loan term: Are you using a thirty-year fixed-rate mortgage loan or a fifteen-year fixed-rate loan? This volition have a big impact on how much firm you can afford

- Interest charge per unit: You won't know your mortgage charge per unit for sure until you go loan estimates from multiple lenders. The default shown on our calculator is an boilerplate charge per unit on the day y'all visit; yours will be higher or lower, depending mainly on your credit, down payment, and debt brunt. And then adjust as all-time you can

- Down payment: Your downwards payment affects your involvement charge per unit every bit well as your overall home-buying upkeep. Assume you'll demand at least 20% of the purchase price to get approved for such a big loan

- Other homeownership costs: Estimate your future homeowners insurance premiums and holding taxes. The numbers in the reckoner are country averages. And add together in monthly homeowners clan dues, if you're buying in an HOA'southward expanse, or private mortgage insurance payments (PMI), if you lot're putting less than 20% down on a conventional loan

Recall, a estimator can only requite you an estimate. To know whether you can really afford a i-2 one thousand thousand dollar home, you lot'll need to get preapproved by a mortgage lender.

Preapproval ways the lender has verified your credit, income, savings, and other items on your application.

If you accept a preapproval letter in hand stating you tin can afford a million-dollar home, then it's more or less a sure matter. (Unless any of your financials or mortgage rates change essentially prior to purchase.)

Don't forget almost homeownership costs

And so far, we've only looked at the purchase price for a million-dollar business firm.

We've explored the principal (repaying the sum you borrowed) and involvement on your mortgage. And we've taken into account your likely holding taxes and homeowners insurance.

Simply there are plenty of other costs associated with owning a home — especially with high-value real manor. And you'll demand to budget for these also.

- Closing costs: 2%-v% of loan amount

- Property taxes: most one% of home value

- Homeowners insurance: $100-$200 per month

- Utilities: average of $1-$2 per square foot

- Maintenance: variable cost

Closing costs

People oft think near their home buying upkeep in terms of downwards payment. For a $1 million home, you lot're likely to demand a minimum of $100,000 to $200,000 saved for that purpose.

But a down payment isn't the but thing to save for. Habitation buyers take to consider endmost costs on their dwelling purchase, also.

Closing fees typically offset around two% of the buyer'south loan amount.

Then if you lot're borrowing $800,000 to buy a million-dollar house, your closing costs could exist around $16,000 or more than. You lot'll need to gene this number in when thinking virtually how far your savings will stretch.

Holding taxes

Dwelling house buyers as well need to consider their hereafter holding taxes.

Real estate revenue enhancement rates are set by local taxation authorities, and they vary a lot depending on where you alive. But to give you a ballpark guess, the boilerplate national property taxation rate is around 1% according to the Revenue enhancement Foundation.

That means on a $i 1000000 house, in that location's a good chance y'all could pay around $10,000 per year in belongings taxes. That's over $800 per month.

Research holding taxation rates where you plan to purchase and make sure y'all factor this toll into your upkeep for ongoing housing costs.

Homeowners insurance

Homeowners insurance is probable to be more expensive on a larger abode, too. The typical homeowner might spend $50 to $75 per month to insure a standard dwelling.

But a larger dwelling house costs more to replace if it is destroyed past fire or another disaster. Naturally, the insurance company will accuse more than for greater risk.

Await to pay $100 to $200 per month to insure your meg-dollar home.

All in, you could pay $1,000 per month in taxes and insurance, a sizeable beak above and beyond the principal and interest payment.

Running costs, repairs, renovations and maintenance

The bigger your home, the more it costs to run. The larger square footage and perhaps higher ceilings that you loved, mean you have a larger book to oestrus and cool. So your utility and HVAC servicing bills are going to exist a lot college.

While utility costs vary by location, as a rule of pollex, you lot can approximate on paying betwixt $ane-two per square foot.

A bigger home besides means more to clean and maintain — and often comes with a yard that will require upkeep.

In short, keeping a large, expensive dwelling well maintained isn't inexpensive. And neither are renovations and repairs. So plan ahead and make sure your home ownership budget leaves yous with a sizeable cushion in your savings account.

Benefits of buying a $1M house

Your ongoing costs may be higher with a bigger home. Simply the benefits to your net worth should typically exist greater, too.

Indeed, domicile toll appreciation averaged xv% throughout 2021 according to CoreLogic.

That ways if your dwelling house was worth $500,000 in 2020, it was likely worth $575,000 or more at the end of 2021 — netting y'all a $75,000 habitation disinterestedness gain.

And for a million-dollar home? Prices were up by well-nigh $150,000 year-over-yr on average. So y'all're likely to run across a prissy return on the coin you invest in your house.

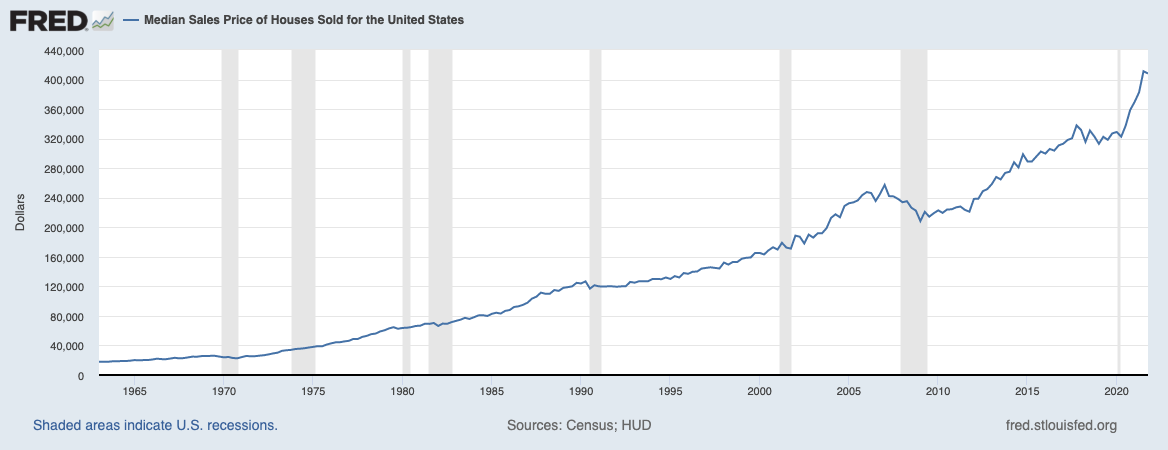

Of grade, all this relies on home prices continuing to ascent. And we all know that they very occasionally fall.

But accept a look at this graph from the Federal Reserve Bank of St. Louis:

Source: U.Due south. Census Bureau and U.Southward. Department of Housing and Urban Evolution data via St. Louis Fed

You can see how rare it is for home values to decrease — and how strong the overall upward trend is.

You lot might call up real manor is non a bad place to accept $one million invested.

What are today'south mortgage rates?

There'due south i other trend prospective habitation buyers should pay attention to, and that's mortgage rates.

Depression mortgage rates heave affordability. Simply when rates rising, it can be harder to afford a dwelling at the loftier end of your budget.

Then it's worth looking into financing sooner rather than later on if you're serious near buying a $i meg home. And do all you can to shore up your credit score and savings earlier applying.

The information contained on The Mortgage Reports website is for informational purposes only and is not an advertisement for products offered by Total Chalice. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Chalice, its officers, parent, or affiliates.

Source: https://themortgagereports.com/71443/income-to-afford-1-million-dollar-house

Posted by: rochaunpleted1961.blogspot.com

0 Response to "How Much Money You Have To Pay A Month In Mortage For A Million Dollar Home"

Post a Comment